Report from the Field & Other Thoughts: Visit to Monterrey Mexico for INCmty November 15, 2022

The Disciplined Entrepreneurship Toolbox

Stay ahead by using the 24 steps together with your team, mentors, and investors.

Sign up for our newsletter

In my all-consuming job at MIT, it is very easy to just stay in Cambridge, keeping busy and feeling satisfied. It takes some effort to overcome the inertia to get out and see what else is going on, but when I do, I always enjoy it and learn something new.

This past week I took a trip to Monterrey, Mexico for the 10th Anniversary of the INCmty Festival to support the amazing Monterrey REAP Team. MIT REAP (Regional Entrepreneurship Acceleration Program) was started by Scott Stern, Fiona Murray, Ed Roberts, and I in 2011 to bring a systematic and disciplined approach to the question we got all the time, “How do we build an entrepreneurial ecosystem like you have at MIT?” Over the years we have had many participants; 51 regional teams in 7 cohorts.

Building an innovation-driven entrepreneurial ecosystem is incredibly hard and the landscape is littered with unsuccessful attempts (see Josh Lerner’s Boulevard of Broken Dreams). It takes a multi-stakeholder approach (entrepreneurs, academic institutions, risk capital, government, corporates) while simultaneously keeping the entrepreneur at the center of every discussion, which sounds easier than it is in practice. Because it is hard and takes a long time to make progress, REAP is two years in length, which requires a long-term commitment from the teams as well as a long-term vision coupled with short-term and medium-term milestones to ensure progress toward the ultimate goal.

While many have gotten enormous value out of the program, no one has gotten more than the diverse and vibrant team from Monterrey. They have utilized the program as an opportunity to build connective tissue across the various players in the ecosystem to the level that, two years after the program’s formal completion, the various stakeholders still get together every week for an hour to discuss progress, issues, and plans going forward.

Monterrey is the second or third largest city in Mexico (depending on who and when you ask) that is a two-hour drive from the U.S. border. It has become a global hub of industrial manufacturing excellence – sometimes referred to as the Detroit of the South. It is also blessed with the great academic institution, Tecnológico de Monterrey, which was patterned after MIT and is very practical and equally entrepreneurial-focused.

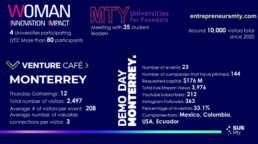

The region is an area that started from a strong base but was humble enough to say it could and must do better. As they worked through the two years of REAP, they made extraordinary progress. Here is a highlight of some of those accomplishments from Dr. Antonio Ríos Ramírez’s presentation at INCmty:

But after they finished the program with these accomplishments, they were not satisfied. They knew that they could and should do more. They understood that entrepreneurial ecosystems are not a zero-sum game, but rather follow the rules of Metcalfe’s Law: that the more entrepreneurs and entrepreneurial ecosystems there are and the more they are connected, the value to each node on the network grows exponentially bigger (based on the number of quality nodes) and everyone gains.

As a result, they set out to take their new-found knowledge and experience and roll out a domestically focused REAP program for five regions of the country – MIT REAP Focus Mexico. Today they are running this program and the regions (including Mexico City, Guadalajara, Chihuahua, Guanajuato, and Queretaro), and everyone is working together and benefiting greatly. While I was in Monterrey, I was fortunate to be able to experience first-hand being in a room with the teams and seeing them working together. The atmosphere and energy were electric.

INCmty is just one of the REAP initiatives and this one was led by risk capital stakeholder Rogelio de Los Santos, who won a community award at the conference for his selfless and effective efforts. “INC” stands for Innovation Networking and Creativity and “mty” stands for Monterrey. The festival is now in its 10th year and has grown such that this week it had thousands of participants.

I was deeply honored to be able to come and support the cause by giving a supportive speech at this conference with my friend and Monterrey REAP team member, Dr. Antonio Ríos Ramírez. My talk focused on the past, present, and future of innovation-driven entrepreneurship. It was a chance to reflect on the arc of entrepreneurship over my career starting in 1980 to today and to look forward to what comes next. Things have progressed from when I first started when entrepreneurs were considered eccentrics. The nature of entrepreneurship was fundamentally commercializing R&D primarily driven by Moore’s Law at a relatively slow and manageable pace relative to today’s mind-blowingly different world.

Today is a world where entrepreneurs are pretty much universally admired. They are essential antifragile leaders in a world that is being disrupted at a dizzy rate resulting from the combined and compounding effects of not just Moore’s law but also Metcalfe’s Law, Andreessen’s mostly fulfilled promise of the digitization of the world with software, and now the almost frightening pace of progress relative to Data, Data Analytics, and Machine Learning (really just getting started). It was fun to think about this arc of history and what it means going forward. It is the first time I have done this talk and one I am going to work more on, starting this coming week at the FLY ASIA Conference in Korea (via Zoom).

Spoiler alert, all of this means we need more entrepreneurs, and higher quality entrepreneurs who are better connected (note: that is generally the answer; not sure what the question is, but that is generally the answer).

A point of the talk that was particularly relevant to the context of this event is that the problems we face as businesses and society are getting bigger and bigger and so we also increasingly need more than startups going forward. We need entrepreneurs who can scale. So, within this environment, the MIT REAP Monterrey team announced the launch of Monterrey Scale Up Nation (notice the play on Israel’s Startup Nation theme – clever, no?).

Again from Dr. Antonio’s presentation, here is a high-level description of the program:

What does this translate to? The creation of more entrepreneurs with scaling capabilities. That being said, it is critical to measure results to produce a focus on achievement rather than activity and the Monterrey REAP team understands this. They have identified 3 priorities towards this end:

- Golden Flag: Building strong connections with partner cities in Texas that geographically form a flag – Houston, Dallas, Austin, and San Antonio. They do not intend to go it alone (very smart) but work with others. This is one of the most powerful economic drivers in the world today and rather than compete, Monterrey is taking the intelligent approach to collaborate.

- Tech companies in MTY: They are going to measure their program with a dashboard beginning with data points they can capture and grow their KPIs from there. These include:

- # of IDE companies

- # of IDE entrepreneurs

- $ IDE financing

- $30B from IDEs: Ultimately, the goal in 10 years is to have almost a third of the revenue from their region coming from IDE companies. Today, they do not even measure it, but they are sure it is a small fraction of this goal. The $30B target is bold and just the kind of motivation the region needs.

Importantly, the team has not just set goals but determined a plan, funding, and a governance structure to achieve this transformational goal.

Will they hit these goals or exceed them? I don’t know for sure but I do know I would not bet against them based on history. I also know that setting such BHAGs (Big Hairy Audacious Goals) is what all of us should be doing now as we see the challenges ahead. I am so proud of the Monterrey REAP team and so happy to have been part of the journey. Thankfully it is not done yet. Stay tuned.

Special Thanks to Blanca Flores for making the visit so productive and drama-free. And to Patricio Villareal and Sofia Castillo for five-star driving and great conversation. Also, to Victor Trevino for a wonderful dinner and conversation on how corporates can help not just with IDEs, but also with climate change.

Special Thanks to Blanca Flores for making the visit so productive and drama-free. And to Patricio Villareal and Sofia Castillo for five-star driving and great conversation. Also, to Victor Trevino for a wonderful dinner and conversation on how corporates can help not just with IDEs, but also with climate change.

Final Important Note:

While I travel less these days, it is always so rewarding to meet former students who have put the “Disciplined Entrepreneurship” methodology to work to create jobs and make the world a better place. There were several at the conference whom I took pictures with, but would love to hear your stories in more depth (please share them here or wherever you feel most comfortable). That is not just how we learn but also gives us the extra energy to keep pushing forward. I know I missed you Mercedes Bidart, but am so happy for your success in creating more financial inclusion in LATAM with Quipu. Keep up the great work and help us spread the knowledge to make more, higher quality, and better-connected entrepreneurs throughout the world. Just yesterday I had the great pleasure to meet Hugo (never got his last name) on the subway here in NYC. When he first came up and introduced himself, he apologized for just anonymously walking up and saying hello and telling me had taken the Entrepreneurship 101 course. He recognized me and wanted me to know that while he had not yet started a company, it has given him the confidence to be more entrepreneurial, and someday he wants to and believes he can. I had to correct him and ask him not to apologize, but instead, thank him for taking the initiative. It is so rewarding to hear. Thank you to all who make the educator feel good about what we do. It is the ultimate reward.

And some extra materials (an illustration created based on my talk and a press review in Negocios):

The author

Bill Aulet

A longtime successful entrepreneur, Bill is the Managing Director of the Martin Trust Center for MIT Entrepreneurship and Professor of the Practice at the MIT Sloan School of Management. He is changing the way entrepreneurship is understood, taught, and practiced around the world.

The books

This methodology with 24 steps and 15 tactics was created at MIT to help you translate your technology or idea into innovative new products. The books were designed for first-time and repeat entrepreneurs so that they can build great ventures.

How Well is MIT Really Doing at Creating the Next Generation Entrepreneurs?

The Disciplined Entrepreneurship Toolbox

Stay ahead by using the 24 steps together with your team, mentors, and investors.

Sign up for our newsletter

A Critical Analysis Through the Lens of the Oct 31, 2022, Pitchbook’s Ranking of Universities Based on Entrepreneurial Output.

How does one assess the effectiveness of one’s educational programs? This is an incredibly hard problem in any case especially when it comes to entrepreneurship education. There are so many contributing factors it becomes impossible to know for sure. That does not mean we should give up. We must strive to constantly look for data points to objectively provide feedback on the reality of how well we are serving our mission.

In this regard, the just released “Pitchbook Study of Universities: Top 100 colleges ranked by startup founders,” by Jordan Rubio & James Thorne provides one relevant and insufficient benchmark. While I have an immediate negative reaction to rankings in general (we should never pit entrepreneurship educators against each other, we are all in this together), this one is extremely data-driven with a powerful data set that Pitchbook has been able to accumulate and does not have ambiguous formulas to determine ranking. Jordan and James are very transparent and even give filters to look at the data, which will come in very useful.

This study provides a benchmark to give a sense of how the overall output of various top institutions. There could be a list of weaknesses hundreds long of what this fails to capture (I will highlight some later) but because we get a view of the raw data, I would like to make a few observations and add to the dialogue.

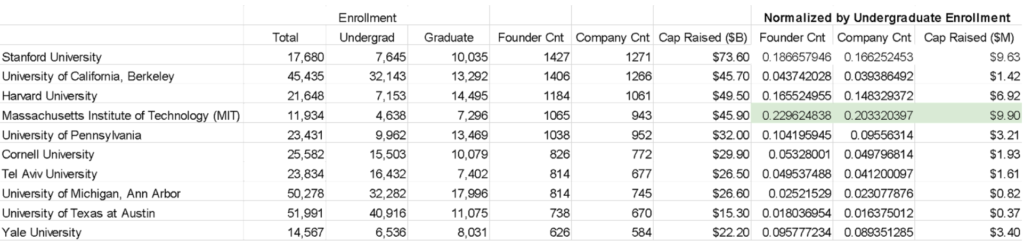

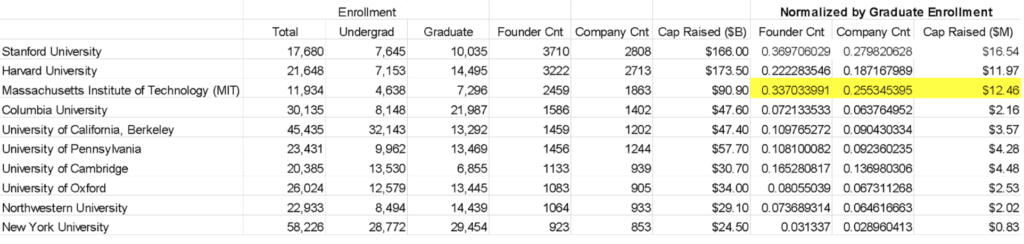

On a first pass of the numbers, thinking about ourselves, we are in great company. MIT ranks 4 in undergraduates, 3 in graduates, 6 in female founders undergraduate, and 3 in Female founders graduate. That being said there is another way to interpret the data that I am immediately left wanting. What I want to see is these results in some ratio relative to the total population. In that way, we could compare like to like. Think of this as the density of VC-backed founders (as a proxy, imperfect as it might be) per institution. I have not seen this before and wished we could normalize the numbers, and we have made a first pass at this below.

But even before this is done, the beauty of this study is that Jordan and James have given us a first step in this direction because in the filters, you can see “Total Enrollment” as the second filter and there are three options: “15,000 or fewer students,” “15,001 to 29,999 students,” or “30,000 or more students”. When you click on the filter to look at the institutions of 15,000 students or less, MIT is the clear #1 leader in all of these by a wide margin (on average 2.3 in number of founders who raised). This aligns more with what we see on the ground. The MIT ratio would be very high. Is it the highest? We don’t know for sure but normalizing the numbers makes me feel like this is a much more valuable benchmark. Well, when we discussed this at our center and everyone agreed. In fact, one of our EIRs, George Whitfield, took the initiative to utilize publicly available numbers and do this normalization.

This yielded the following (unaudited) results for Undergraduates:

Likewise for Graduate students:

Note: We did not have a data set we were comfortable with regarding the dimension of women founders which is important to provide insights into the inclusivity of the entrepreneurship education programs so that can be a later exercise.

This is in no way saying that these are the only KPIs or the key KPIs to measure our success, they are not in our opinion. It is but one data point that is flawed in so many ways. Does this mean that MIT and Stanford are the best? No, that is not what we are saying and we know that we are imperfect and always strive to get better in any case. In fact, the ranking mentality of pitting educational institutions can have a positive side to benchmark what is working but it also can have a very dark side. Entrepreneurship educators must work together. This is not a competition between each other. We have a common goal. The competition is against bad or no entrepreneurship education. We radically share and open source everything we do. That is what we all must do if we are to advance the field in the manner it needs to so as to address the challenges we face as a society.

That being said, it is good to have objective measurements of how we are doing—this is one data point and it is heading in the right direction. I wish it would go a step further to normalize the numbers based on student population size. It would still not at all be the singular or even most important metric to measure progress, but it would be a proxy for progress and success.

What are some of the other areas for improvement in this study?

- Assumes that VC-backed founders are a proxy for success. We know this is not the only path to success. Entrepreneurs may not need to get nor should they seek VC funding to be successful.

- We do not know the success rate of these companies, rather we just know how much they raised.

- It does not normalize for input. Maybe MIT students would have raised money and been successful no matter what we did?

- Which raises the question, how much a difference did we really make? Did we instill an entrepreneurial mindset into them? If so, how much? How much did we improve their skill set? How much did we improve their ability to operate like an entrepreneur in a community-based manner with resources beyond their control?

- Ultimately, we as educators should have a goal (i.e., teaching objectives) that we instill in our students (e.g., mindset, skill-set, and way of operating per point #4 above) and measure our students before and afterward to determine the progress made in all of these categories.

- In this ideal scenario, we would be able to measure the positive progress in the key areas mentioned above in #5 and our entrepreneurs would thrive as founders but also as entrepreneurs joining startups and also as entrepreneurs in existing organizations (government, academic, corporate, government, non-profit or others) and we won’t have to rely so heavily on numbers like those in Pitchbook but until then we have to work with what we have and keep making it better.

I would also note that recently we completed a ten-year empirical research study of the success of our delta v program that relates back to this topic of assessment and those extremely interesting results are available here.

Assessment will continue to be the 800-pound gorilla in the room for entrepreneurship education in my opinion. How do we know what we are doing works? To know, we have to have measurements and while there is some work done in this area, there is so much more that needs to be done to differentiate the effective from the ineffective… and do more of the effective. Like most other things in entrepreneurship, we can’t wait for the perfect, we have to go with what we have and keep improving it.

Afterword: I wrote this up and then read an email from my original mentor at MIT, Professor Ed Roberts, who had done numerous landmark studies on the impact of entrepreneurship and he had done a similar analysis so I guess I was trained well.

The author

Bill Aulet

A longtime successful entrepreneur, Bill is the Managing Director of the Martin Trust Center for MIT Entrepreneurship and Professor of the Practice at the MIT Sloan School of Management. He is changing the way entrepreneurship is understood, taught, and practiced around the world.

The books

This methodology with 24 steps and 15 tactics was created at MIT to help you translate your technology or idea into innovative new products. The books were designed for first-time and repeat entrepreneurs so that they can build great ventures.

DE Teach The Teachers (T^3) Workshop (Mexico City, Nov 17–18)

The Disciplined Entrepreneurship Toolbox

Stay ahead by using the 24 steps together with your team, mentors, and investors.

Sign up for our newsletter

I am super excited to announce a special workshop for educators on how to teach Disciplined Entrepreneurship to be held on November 17–18 in Mexico City. It will be run by Instituto Tecnológico Autónomo de México and more specifically the EPIC Lab and Daniela Ruiz Massieu in collaboration with the Martin Trust Center for MIT Entrepreneurship‘s own Jenny Larios Berlin. It will be useful for many but it will also have a specific focus on LATAM. See below for more information.

We had the great honor to have Professor Ruiz Massieu spend last year with us observing firsthand what we do at the Trust Center with a critical eye. She then jumped in within two months and became a beloved teacher. She then spent the rest of the academic year perfecting the craft of teaching the materials as well as doing research on its effectiveness. She has a particularly important knowledge of how to apply the methodology outside of MIT having taught it for years now as well in LATAM. Jenny Larios Berlin is a seriously experienced young entrepreneur who has tried entrepreneurship many different ways (including most famously with the impressive and successful Optimus Ride experience) and is now a full-time Entrepreneur In Residence (until she is ready to jump into her next big entrepreneurial initiative) and Lecturer at MIT teaching the methodology numerous times every week. Both offer invaluable knowledge and perspective on how to teach the Disciplined Entrepreneurship methodology in the most effective and efficient manner. All materials from the workshop will be made available to the participants making it dramatically easier to empower the participants to teach the materials upon completion.

See the poster below for more info and sign up now, as they have just released seats to the general public.

The author

Bill Aulet

A longtime successful entrepreneur, Bill is the Managing Director of the Martin Trust Center for MIT Entrepreneurship and Professor of the Practice at the MIT Sloan School of Management. He is changing the way entrepreneurship is understood, taught, and practiced around the world.

The books

This methodology with 24 steps and 15 tactics was created at MIT to help you translate your technology or idea into innovative new products. The books were designed for first-time and repeat entrepreneurs so that they can build great ventures.

MIT delta v 2022 Videos Now Available... and More

The Disciplined Entrepreneurship Toolbox

Stay ahead by using the 24 steps together with your team, mentors, and investors.

Sign up for our newsletter

MIT delta v Demo Day 2022 happened on September 9th in from of 1,500 energized MIT students live and thousands more online. What you all are probably most interested in is that the videos are now available for viewing here (there is also a very nice digital version of our Demo Day book summarizing all the teams and the program). Every year, the student teams improve and this year was certainly no exception. We could not be prouder of this year’s cohort and we are absolutely confident they will continue and amplify the strong tradition of delta v entrepreneurs positively changing the world in a big way.

A few headlines of note:

- Women Rule: While the number of participants and CEOs for those identifying as female has been strong from the beginning 10 years ago and rising since, this year marks a watershed in that 50% of the participants identified as female and 55% of the CEOs. You will see this in the videos for sure. If we want entrepreneurship to be the best it can be and the most impactful, we need the biggest tent possible to be inclusive. Very proud of this.

- Back in Person Really Matters: Zoom is good for certain things but for teaching entrepreneurship, it can’t replace the high-touch instruction and mentoring that can be provided in person. Have done the program remotely in 2020 and then hybrid last in 2021, you could just see the energy at a different level. More importantly, we saw first-hand that the improvement of the teams was at a much faster rate in person and we got a lot more done this year than last year. So much more rewarding for the educators and mentors running too. There is a role at times for Zoom but for a fully immersive acceleration program teaching entrepreneurship, thank goodness we are back in person.

- Trust the Process: We have always focused on developing the entrepreneurs much, much more than the companies that they are creating in delta v summarized by the statement “companies << entrepreneurs”. We stand by this statement completely because the entrepreneurs are the ones who create the companies and if we teach them how to do so (“teach them how to fish”), they will create multiple companies (“catch many fish”). This year I realized that there is something even more important than entrepreneurs, wait stay with me, and it is the process of creating entrepreneurs. After 10 years of delta v and seeing us start from raw students who don’t have an idea, a team, and certainly not a company one year earlier, and each year take them from a standstill (“0 miles per hour”) and by the end of delta v (note it is more than delta v in that the full year program includes the t=0 festival, courses, fuse micro-accelerator, co-curricular programs) these same students are legitimate entrepreneurs with exciting teams, plans and customers (“15 miles per hour”) never fails is the real gold here. To put this in simple terms, I love new mission-driven economically sustainable companies but I love even more high-quality innovation-driven entrepreneurs but most of all, I love the process to create these entrepreneurs because that has the biggest force multiplier effect of all. In other words: companies << entrepreneurs << process of creating entrepreneurs.

- Impact Study: We had the fantastically great fortune of having Professor Daniela Ruiz Massieu, who is the head of entrepreneurship at ITAM in Mexico City, on sabbatical at our center this past year and she did a longitudinal study of the impact of delta v after 10 years. The results were stunning. Even going back to the beginning ten years ago, the companies that were started in delta v are still operational (or were acquired) at a rate of over 60% and if you look at the past five years, that rate is closer to 70%. The amount of money they have raised is over US $1 Billion for these companies. Again, remember they started from scratch. 38% have gone on to other accelerators like Y Combinator, TechStars, and MassChallenge. One of the most interesting statistics in my estimation is that participants have gone on to found another 120 companies that we can identify and they have raised over US $2 Billion. This reemphasizes the educational mission of our accelerator that we are teaching them how to create companies rather than creating one company. You can see a summary of the report here (https://entrepreneurship.mit.edu/delta-v-10-year-study/) and we hope to have a full report out soon. Deepest appreciation to Daniela for doing this very important research.

There is so much more but I think the best thing you can do now is go and watch the videos of the students presenting. They are so inspirational and we hope they will inspire others as well that “Yes You Can!”

The author

Bill Aulet

A longtime successful entrepreneur, Bill is the Managing Director of the Martin Trust Center for MIT Entrepreneurship and Professor of the Practice at the MIT Sloan School of Management. He is changing the way entrepreneurship is understood, taught, and practiced around the world.

The books

This methodology with 24 steps and 15 tactics was created at MIT to help you translate your technology or idea into innovative new products. The books were designed for first-time and repeat entrepreneurs so that they can build great ventures.

New Academic Year Kicks Off: Additional Examples of Excellence from MIT Students

The Disciplined Entrepreneurship Toolbox

Stay ahead by using the 24 steps together with your team, mentors, and investors.

Sign up for our newsletter

It is a new year and every year we like to continue to update the teaching materials we make available to all Disciplined Entrepreneurship educators. This year we have added examples of excellence in final deliverables that we make available to students in our course at MIT. These final deliverables are concrete examples of what students have submitted at the end of a semester of work. They provide inspiration and a benchmark for others – and students have found it very helpful to see what others have done to help guide them as they work throughout the semester toward their goal of something similar. No path in entrepreneurship or this course is ever the same, nor should they be, so these should not be used as templates that if repeated assure success but rather are imperfect but pretty damn good role models of what success looks like in the end and how achievable it is.

If you do not already have access to the teaching materials, you can gain that by filling out this form. It is free and provides a treasure trove of materials to help you that are open source, meaning they can be used under the Creative Commons licensing arrangement (feel free to use it with attribution and if you produce derivative works, they will be made available for free to the community on the same basis).

This is meant to help achieve our goal of creating more entrepreneurs, higher quality entrepreneurs, and better-connected entrepreneurs globally!

The author

Bill Aulet

A longtime successful entrepreneur, Bill is the Managing Director of the Martin Trust Center for MIT Entrepreneurship and Professor of the Practice at the MIT Sloan School of Management. He is changing the way entrepreneurship is understood, taught, and practiced around the world.

The books

This methodology with 24 steps and 15 tactics was created at MIT to help you translate your technology or idea into innovative new products. The books were designed for first-time and repeat entrepreneurs so that they can build great ventures.

Chapter 3: Financial Modeling (Part 2)

The Disciplined Entrepreneurship Toolbox

Stay ahead by using the 24 steps together with your team, mentors, and investors.

Sign up for our newsletter

What creates revenue?

This should be very simple as in the example I have provided. It should be some “units” time average selling price (ASP). ASP is the average amount of revenue that you receive per unit. This is after discounts and commissions you pay to resellers. It is the actual money that flows into your bank account.

What do you mean by “Units”?

This can be a bit trickier than it might first appear. Units can be the number of products sold.

However, it could and more properly (for future calculations) should be one average customer. If an average customer buys only one product, then these two are the same. On the other hand, if an average customer buys 2 products, then they are not the same. The model would get a bit more complicated like below:

You are probably thinking, why does it matter? It does. As we get later and we are analyzing our marketing and sales costs, we are going to do it on a per customer basis as opposed to a per unit basis so we need both the number of new customers (for the future) and the number of new units (for now).

What is the average revenue per unit?

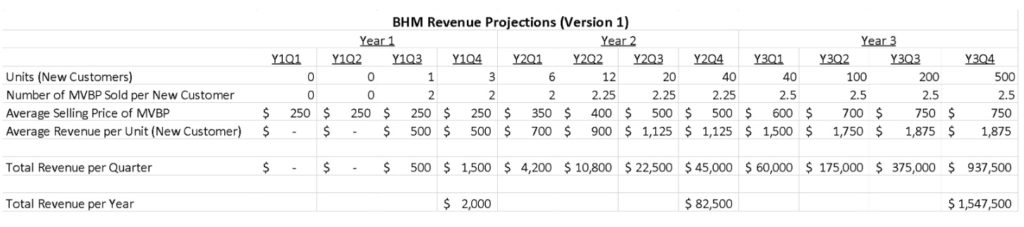

In the case above, the average revenue per unit is based on the customer. Let’s look at one quarterly example for the first quarter of the second year. The ASP for the product this quarter is $350 but since the unit is an average new customer, the average revenue per new unit is $700. This is because, in this quarter, we are projecting that, on average, a new customer will buy two of our products.

This may seem a bit more complicated but it is important to set us up to understand the unit economics involved with LTV (Life Time Value of an average customer) and the COCA (Cost of Customer Acquisition or also often called CAC, Customer Acquisition Cost). These are important lenses through which to analyze our business and we want to make sure our model is aligned with them.

It is helpful to see the size of the total BHM in units/customers so you can quickly understand market penetration

Another piece of information that you should have available and I actually like to include in the modeling is the size in units of the target market you are addressing. This should not be your basis for calculating your revenue projections (that should be “bottoms up” with specific customers) but rather a “sanity check” that they are reasonable.

In this case, it is the BHM and not the overall market (we will add the overall market later once we have this done).

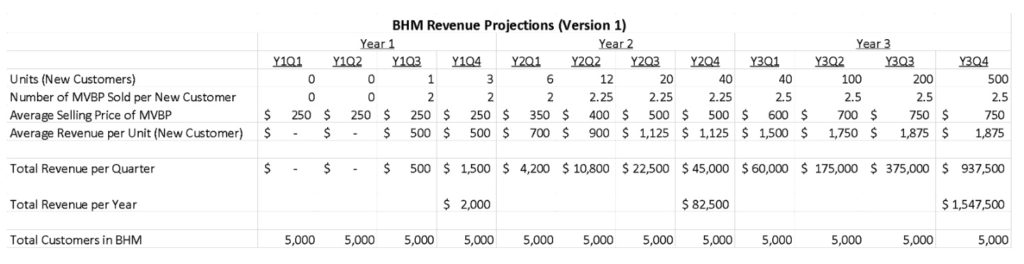

As you can see now in the last row, there are an estimated 5,000 customers in their BHM so getting 500 in a year is put in a much more concrete perspective. Is 10% reasonable in one quarter or not? It depends on the nature of the market. This number also tells you that by the end of year three you expect to have over 900 customers within this market which is almost 20% of the market. Is that reasonable or not? It depends on the marketplace dynamics and the strength of your product but this number gives important context.

It also gives an indication of when you will reach saturation in a market, in this case, your BHM.

There can be a case made to not crowd the spreadsheet with this number but rather note elsewhere, e.g, footnote, comment, backup, or verbal comments. There certainly is a benefit to keeping things simple but whether it is on the spreadsheet visible in your model or not, you need to know this number and explain it at some point.

Level of Precision

As mentioned before, critics of models will say “they are never correct!.” That is true from a precision standpoint but it does not mean they are not useful. They can certainly be both not precisely correct and very valuable. However, there is a very valid point that you should not get caught up in a level of precision that you cannot know and such specificity is not useful, like the exact numbers of new customers in the third quarter of the third year. You should come up with a reasonable number and be able to justify it. The closer in time you are to your numbers, the more precision you should have. For instance, if you are projecting the number of new customers in the next 30 days, that number should be quite precise and you should be able to back it up with great specificity. It is still a forecast as it is in the future so it is not a certainty but you should have confidence and resolution that you will not have for a forecast on the number of new customers in year five. In year five, it is not only a good way away in time but you will also be layering on additional markets beyond the BHM for which you have not done extensive PMR (Primary Market Research).

In the near term, you should have much higher confidence and rely on specific bottom-up information you have collected directly via PMR and selling efforts already underway. In the long term, you will depend more on secondary research. As such, as you get into the out years, make sure you don’t indicate precision on the numbers that you obviously cannot have. You will lose credibility and waste time.

Even in the short term, don’t waste too much time on the precise numbers but rather get to the general numbers and ranges … and what drives those numbers. Remember, your goal is to have a valuable model less than having a precise model. The former is much more attainable in a reasonable period of time and the latter could be a sinkhole of your time for something that will never be possible. All of this being said, build a good defensible model that explains your business and don’t use the “it will never be right” excuse to not build a useful model.

How do items in our model vary over time?

So far, we have only discussed how a few things would vary over time, like the ASP for the product. If things are not going to change much, you can just leave them constant but if they are going to change materially, you should look at incorporating positive or negative growth rates. The ASP showed a positive growth rate in the simple example model we have been discussing as we gain pricing power from our customer successes. We also see the number of units purchased by customers increasing, as they get more confident in our solution.

What could experience a negative growth rate? The number of customers in our target market might decrease due to consolidation or other market factors. We might see a decrease in ASP as competitors flood the market after they see our success or our patent expires. I would encourage you to not get caught up in these things at first as you build your model but leave the ability to add them in later as you refine your model.

What is the lifetime of a customer and/or product?

As you build your model, other questions will continually arise but one that will arise very quickly is, “what is the lifetime of a customer and/or product in your situation?” How long you will retain a customer will affect the follow-on revenue that you will get from that customer. This includes whether they will be a replacement product if the current product becomes obsolete from use or advancement of technology. Think of the Apple iPhone. If you are a loyal customer of theirs, the product lasts about 3 years (give or take). If they stay a customer, that means they will buy a new product from you every 3 years on average. That would then also be built into your model. This leads to the discussion of retention rates and churn, which become very important as your model becomes more sophisticated, but you don’t need to worry about this now at the beginning but know it is coming.

What if I have a different type or type of business model to generate revenue? (e.g., one-time charge, recurring revenue, transaction revenue)

What you do need to know at the beginning is the various types of revenue. This model assumes only simple “one-time charge” revenue. That is very nice in that it makes the model easy. It is also well accepted by customers and the most common form of revenue. This however does not mean it is the only and certainly not necessarily the best for you and your customer. In fact, the “one and done” model has some problems but it will never go away.

The “recurring revenue” business model or subscription model has become very popular driven by the boom of SaaS (Software as a Service) and its successful evolution. It is here to stay and investors, customers, and vendors generally love it. It has even spread to other non-software industries. It produces a steady stream of revenue for your venture that is predictable and robust against recessions and other economic fluctuations. Investors value this type of revenue much more highly than one-time revenue and customer may like the fact that they don’t have to pay upfront and they can depend on continual updates to their products. They may pay more in the end, potentially meaning a higher LTV, but they often are willing to do so.

Another major business model is the transaction business model where the customer pays based on their usage. Think of an electric utility and how it charges us. The consumables business model is also really a variation of this. You buy the razor but the more you use it, the more blades you use. Likewise for your printer. The more you use it, the more ink you buy. Again, for a certain customer base, this is very attractive and generally accepted as the norm of business.

This has not been incorporated into our simple model but it could be as below as another section like the “One Time” and “Recurring Revenue” sections.

Notice that you can combine business models, and businesses often do. The customer, in this case, is paying upfront for the product but they also pay a maintenance fee, which generates recurring revenue. In this case, the recurring revenue is proportionally small compared to the one-time revenue ($64K vs. $937K) but it can be much larger for other businesses. As stated previously, the recurring revenue has many very attractive characteristics and is highly valued by entrepreneurs and investors so don’t overlook this source. You should also look to think of creative ways to increase this stream of revenue.

It is definitely simpler if it is only one type of business model and if you had your choice, you would likely pick the subscription model. It would make the modeling much easier. That said, the subscription model is not without its weaknesses and each business model has its strengths and weaknesses. You have to find the best mix for your situation.

Also note that there are other business models that would make your financial revenue model more complicated like advertising, affiliate marketing (e.g., getting commissions), selling access to data, franchising, and more (see step 15 of the Disciplined Entrepreneurship 24 steps for a lot more details). All of these could be modeled and the principles are the same but it just gets more complicated.

The author

Bill Aulet

A longtime successful entrepreneur, Bill is the Managing Director of the Martin Trust Center for MIT Entrepreneurship and Professor of the Practice at the MIT Sloan School of Management. He is changing the way entrepreneurship is understood, taught, and practiced around the world.

The books

This methodology with 24 steps and 15 tactics was created at MIT to help you translate your technology or idea into innovative new products. The books were designed for first-time and repeat entrepreneurs so that they can build great ventures.

DE Workbook Worksheets Now Available in Digital Form

The Disciplined Entrepreneurship Toolbox

Stay ahead by using the 24 steps together with your team, mentors, and investors.

Sign up for our newsletter

There was a lot of good material and updates in the red Disciplined Entrepreneurship Workbook which came out after the original white Disciplined Entrepreneurship book that had a chance to be digested by the public and myself. There is a lot of very good material in the book, like the guide on primary market research, the DE canvas, new material on windows of opportunities & triggers, and more that I do not want to trivialize.

The thing I get asked most about is whether the worksheets can be made available in digital format. So here they are and also with a few other good things that I use in our classes each year that you might find interesting and helpful as well.

PS—Please let others know this material is now available.

The author

Bill Aulet

A longtime successful entrepreneur, Bill is the Managing Director of the Martin Trust Center for MIT Entrepreneurship and Professor of the Practice at the MIT Sloan School of Management. He is changing the way entrepreneurship is understood, taught, and practiced around the world.

The books

This methodology with 24 steps and 15 tactics was created at MIT to help you translate your technology or idea into innovative new products. The books were designed for first-time and repeat entrepreneurs so that they can build great ventures.

EDP+ Innovating On How We Teach Entrepreneurship and Grow the Community

The Disciplined Entrepreneurship Toolbox

Stay ahead by using the 24 steps together with your team, mentors, and investors.

Sign up for our newsletter

For well over 20 years, the MIT Entrepreneurship Development Program (EDP) has been the largest and most highly rated Executive Education program offered by MIT Sloan. Think about that for a second as it is quite an achievement. “Executives” are usually looking to take courses to help them become better leaders in big corporations and what we teach in EDP is entrepreneurship! And among all the excellent courses taught by fabulous MIT professors in MIT Sloan Executive Education’s portfolio, our humble EDP ranks the highest.

But success always has an expiration date on it. Like our friend Alberto Rodriguez de Lama of The Cube in Spain and a member of the EDP community likes to say, “Always in beta, always improving.” So this year we made some significant changes to experiment with new ideas. We kept the good we know works and made the following changes for what we called “EDP+”:

- Timing: Since its inception, EDP has run in January. We joke we do this to keep the participants focused and make sure we only get the most serious people in the program. After all, it can be really cold in January in Boston. The real reason is this is the window in our academic calendar where the program fits best. EDP is a fully-immersive environment that requires a full-time dedicated core faculty team for a full week. This year, the innovation in #2 below allowed us to run the program the first week of June for the first time ever. Yes, there were more distractions (Red Sox games, concerts, Celtics games, just going outside in the gorgeous weather, etc.), but it still worked out really well. Because it was early in the summer, we were also able to get key faculty to participate as well.

- Integration with MIT Students: For the first time I believe in any MIT Exec Ed program, the participants were in the same classroom and sharing breaks with MIT students who were learning and applying the same content. These were not just any students either; these were the best, the brightest, and the most committed entrepreneurial students at MIT, the delta v summer accelerator teams. While this sounds great, there were some risks with this plan. First, it has never been done before, but that does not scare us as entrepreneurs. Second, they were at different starting points. The EDP participants were starting from nothing with no idea, no team, and little to no knowledge of the Disciplined Entrepreneurship process. The delta v teams had all of these things and momentum coming into the week. Third, there was a significant age and experience gap between the two groups.

- Even More New Content than Usual: Every year, we look to enhance our content and integrate new materials, but this time, we did this in two critical areas. The first was to integrate the strategy, frameworks, and tactics that entrepreneurs should consider as they develop their “Go-To-Market” plans taken from our new course at MIT. The second was to integrate into EDP key material from another new course, Paul Cheek’s “Venture Creation Tactics”. While this was material that has been tested during the school year, it was extremely leading edge, very actionable, and went beyond the traditional 24 Step Disciplined Entrepreneurship framework. It was more new material than we would traditionally integrate, but we felt it was important to equip the participants with the latest in the field.

Because of these changes above, we positioned this version of EDP as a new experiment, as “EDP+,” and charged ahead to run it while anxious to see the results. As anyone who has attended EDP can attest, this course is like no other program. After 6 days of fully-immersive entrepreneurship sprinting by Friday, everyone is exhausted, including the staff. I am pleased to say that while everything did not go perfectly (perfect only exists in comic books), at our team debriefing on Friday afternoon we were *very* pleased with how it all went.

Most importantly, the EDP participants and the delta v teams really enjoyed and got extraordinary value out of the program. Here are a few of the posts (I am sure I have missed a lot, but please add the missing ones in the comments):

- “10 Things I Learned in EDP+” from the Tie Guy https://www.linkedin.com/feed/update/urn:li:activity:6940702979356307456/

- “Great Artists Ship” https://www.linkedin.com/feed/update/urn:li:activity:6941152446693949440/

- “Life-Changing Experience” https://www.linkedin.com/feed/update/urn:li:activity:6941483147129724928/

- “Mind-Blowing What You Can Achieve in a Week” https://www.linkedin.com/feed/update/urn:li:activity:6941423204875812864/

- “Yes You Can” https://www.linkedin.com/feed/update/urn:li:activity:6941508000297701377/

- “Started the week as an explorer and ended as a believer that, taking an idea and commercializing it, is a craft that can be taught.“ https://www.linkedin.com/feed/update/urn:li:activity:6941568760440901632/

- “My Cliff Notes from EDP+ https://www.linkedin.com/feed/update/urn:li:activity:6941759839056408576/

Anyone who has taken EDP is part of the EDP community and will never forget the experience. Know you are part of a special collective. One of the questions we get most often about the program is can we run it twice a year, and until now the answer has been “Heck No!” However, with these latest modifications, maybe we can and expand our community. That would be wonderful.

Special shout-outs to the MIT Executive Education team, especially Ann Marie Maxwell and Peter Hirst for believing this was possible. Also to the Northern Ireland Catalyst program led by John Knapton and Adele Ward for believing in us and bringing your great entrepreneurs over for this experiment. Also to Jennifer Craw, CEO of Opportunity North East (ONE), and Freda Miller of Scottish Enterprise who kept our long-term (10+ years) relationship with Scotland rolling and also brought a wonderful cohort of entrepreneurs to give us a great core to start the class with. And all the rest of the colorful cast of characters from all parts of the world and all walks of life who made the room so vibrant this past week. Hopefully, every single one of you is feeling more antifragile and knows: (1) Yes you are an entrepreneur; (2) Yes you can continually get better at it; and (3) Yes you are now a damn good entrepreneur with your training and you can lead a more meaningful life and put a positive dent in the universe.

Huge thanks to all the instructors and guest speakers, judges, mentors, and others who we had come in including the great Catherine Tucker, Adam Blake, Matthew Rhodes-Kropf, and David Frankel (and his mother). And of course to my co-lead for this course, the fabulous Paul Cheek.

Lastly, enormous thanks to the Trust Center team who helped pull off this intense one-week-long doubleheader – EDP+ and delta v kickoff. The center is nothing without the people who make it all happen. Here is to you!

Onward and upward and if you want more info on EDP, follow the link at the beginning of this post.

Finally, remember, while we joke around and have fun in EDP, what we are doing is so important. While we should not take ourselves very seriously, we must take the bigger mission very seriously. The world desperately needs more entrepreneurs, high-quality entrepreneurs, and better-connected entrepreneurs. Keep your eyes on the prize.

#donnachisholm #nicoladouglas #HIE

The author

Bill Aulet

A longtime successful entrepreneur, Bill is the Managing Director of the Martin Trust Center for MIT Entrepreneurship and Professor of the Practice at the MIT Sloan School of Management. He is changing the way entrepreneurship is understood, taught, and practiced around the world.

The books

This methodology with 24 steps and 15 tactics was created at MIT to help you translate your technology or idea into innovative new products. The books were designed for first-time and repeat entrepreneurs so that they can build great ventures.

Chapter 3: Financial Modeling (Part 1)

The Disciplined Entrepreneurship Toolbox

Stay ahead by using the 24 steps together with your team, mentors, and investors.

Sign up for our newsletter

As you have seen on this website, I have been releasing draft chapters for comment from the upcoming Financial Literacy and Fundraising for Entrepreneurs book I am working on. Based on feedback and just looking at the length and complexity of the next chapter, I am now planning to release more bite-sized parts of this next chapter (Chapter 3 – Financial Modeling). In this way, I feel it will be more easily and widely processed and feedback can be more focused. In this vein, here is the first part of Chapter 3 for your review and comment. As always, please don’t feel you have to sugarcoat your comments – “critical feedback is the breakfast of champions” is our motto.

By the way, related to this work, there is now a free online edX course, Fundamentals of Entrepreneurial Finance: What Every Entrepreneur Should Know, taught by myself with my MIT faculty colleagues Antoinette Schoar and Matthew Rhodes-Kropf. I welcome your comments on this too!

What is the purpose of a financial model?

In this chapter, we will teach you how to develop a model to generate projections of your business that provides insights, meaningful projections, a potential path to greatness, and a planning tool. I have heard intelligent people say “meaningful five-year financial projections?!?! – come on! They are surely going to be wrong. How can they be meaningful?”

It is correct that they will be wrong but that does not mean the process of building the model as well as the model itself are not useful and extremely valuable. They will be valuable to you, your team, and other stakeholders. To start with, it will force you to understand what key assumptions you must make to derive the revenue, costs, profitability, growth rate, and other factors that will determine your cash flow – a cash flow that needs to be positive for you to continue to exist. A well-designed model is explicit about what assumptions you are making to build your projections.

The skeptic is correct that all of the model projections will not be 100% correct but they will be correct if all of your assumptions become precisely true, which never happens. That being said, this work in trying to quantify the future will give you great insights into what factors are most critical to your financial sustainability and success – and which ones are less important. You will also have a model and you can adjust to see what the new projections look like as you get more information to more accurately forecast key assumptions. In summary, the thought process and a well-designed model will make it clear what are the key drivers of your business to make it economically viable.

Also extremely important, the model should also show you if a path to greatness is possible, and if it is not, then you shouldn’t do the new venture unless you are willing to give up this hope. There should be some set of assumptions that make your business not just financially viable but attractive and highly impactful. Financial projections help to show if the venture will be able to have the level of impact that motivated you to create the company in the first place. The time, effort, and resources required to build this new venture should be worthy of the opportunity cost it will take to build it. This question is not asked enough by entrepreneurs, educators, and mentors. It is not just enough to survive. You want to maximize your impact.

Making clear what your assumptions are and being able to adjust them to see the impact is central to building a helpful model. It must be simple enough to understand and modify but also capture enough of the complexities of your business.

The Sequencing of Building a Model

Start with modeling the top-line (revenue) and then do expenses.

We will start with revenue first because, without revenue growth, nothing else matters. If you can’t produce sales growth and scale, you can’t solve the problem on the expense side. All revenue curves basically look the same – up and to the right. No shame in that. You don’t want them looking any other way. If they are flat, that is no good. If they are headed downward, run!

Once we have built the revenue model and iterated on it such that we are comfortable with the model’s logic, its assumptions, and ultimately its overall numbers, then we will focus on the costs and build up that part of the business model.

In this chapter, we will build the model in three steps. First, we will build the revenue model to understand revenue growth. Secondly, we will add the costs into the model. Lastly, we will build a summary of the model to make it easy to understand the key points. The last step is very important. You must be able to crisply communicate your financial model, current projections, key assumptions, leverage points to watch for, and the path to greatness.

Building a Revenue Model

Start with your Beachhead Market (BHM)

The first part of building your revenue model should focus exclusively on your beachhead market (BHM). This will make the task clearly scoped and much more achievable. It allows for specificity that you will lose as you move on to other markets that you have less information about. That specificity should give you more confidence you are building your first model correctly.

Later we will add a layer on top of this BHM revenue projections follow on markets but you should begin with a focus on the BHM. It makes the job a lot easier to get started.

When Does Revenue Start to Come Into Your Company?

The first question will be, when do you start to get customers? For some, they can get paid by the economic buyer for the MVBP they produce right away. This can be a good thing because you want to test the customer’s willingness to pay. You can always change (hopefully increase) the price later as you prove your value proposition. As time goes on and you are successful in the market, it also decreases your risk as a vendor which will allow you to raise your prices or more likely, decrease the amount of discount you give out to get a sale. Decreasing your discounts has exactly the same effect as increasing your prices and is generally a better way to achieve the same goal. Your model should be built to allow for increases in pricing (or decreases in discounting but going forward that will be implied) by month, quarter, or year.

Here is a very simple example to show how to get started:

Notice this model is just focused on the BHM which makes the problem much more reasonable to address. Secondly, you don’t have to generate revenue immediately. It will take you a while to develop your product and get your first customers. Once you have that first customer, you will likely have to or want to give them a discount as you work out the kinks in your product with them.

The number of customers will start small as you refine your product and build your value proposition and company capabilities as well as market presence to be a respected vendor. As time goes on, you are able to dramatically increase the volume of customers that you acquire while also increasing the price.

This is due to the increased validation you have received in the marketplace from your initial successful installations (they had better be successful!).

So, in this simple model, revenue starts in the third quarter of the first year. It is not much but it is the starting point. When does the revenue start for your new venture? If you are developing a medical device that requires a lot of technological development, product development, and regulatory testing and approval, this could take years, which is painful but it is what it is. You might have a mobile app that you can put together an MVBP in a matter of a month so you might be able to get your first paying customer within the first month or quarter. As you can see, it will vary widely based on your situation and industry.

How much should I charge at the beginning?

As you can see from the model above, in the beginning, the price is very low ($250) as compared to what it is projected to be three years later ($750). Why is that? This is because at the beginning, you don’t have pricing power and you want to have customers who are more forgiving as you iterate to improve your product. You have not yet proven your value proposition in the market place and you are seen as a risky vendor. Rarely does a person or organization want to be that first customer (it is very risky to be first) so you have to give them some incentive. You would generally do this by giving them a discount. It is almost always easier to have a high list price and give people a discount and then later decrease the discount you are giving people than to raise the price. You can raise the price but you generally want to do this with a release of a new product with a lot more functionality (e.g., iPhone 10 to iPhone 11s with a new camera). Increasing the list price on the same product is a tough sell often to customers as they are conditioned to the previous price. Hence, decreasing discounts is a less conspicuous way to increase prices if you can do it properly.

There can be a case for not charging customers, especially end-users who are not the economic buyers, at the beginning. I must admit, I am not a big fan of this except in extreme cases. You have not proven one of the key elements you need to in an MVBP if you do not charge, that is the economic buyer’s willingness to commit to paying something. If there is no skin in the game and the product is free, have you really proven one of the most important hypotheses of entrepreneurship, i.e., that you can extract rent for the value you have created? No. That is why I am generally skeptical of this approach.

That being said, if your business is a platform or one that depends on monetizing the data collected from lots of end-users, it is virtually impossible to get the economic buyer to pay until you have acquired users. This is really the exception to the rule but it should not be used as a cop-out for others to avoid gaining a commitment from the economic buyer to pay something (it does not have to be full value to start) for the value you are creating.

Behavioral economists have shown it is very hard to get people to pay for things that they have gotten for free historically. It is hard enough to get them to increase the amount they pay but it is much worse to get them to pay anything when they have paid nothing and the mental model they have is that the product or service is free.

So my advice is to charge the economic buyer(s) something as soon as possible and then increase it over time as you prove your value proposition and your company. At a minimum, call it a “free trial period” so you can go back and extract rent at the end of the trial period.

The author

Bill Aulet

A longtime successful entrepreneur, Bill is the Managing Director of the Martin Trust Center for MIT Entrepreneurship and Professor of the Practice at the MIT Sloan School of Management. He is changing the way entrepreneurship is understood, taught, and practiced around the world.

The books

This methodology with 24 steps and 15 tactics was created at MIT to help you translate your technology or idea into innovative new products. The books were designed for first-time and repeat entrepreneurs so that they can build great ventures.

All People Are Born Entrepreneurs, Then Society Takes This Away

The Disciplined Entrepreneurship Toolbox

Stay ahead by using the 24 steps together with your team, mentors, and investors.

Sign up for our newsletter

Interview originally published in Ta Nea (Greek newspaper) on March 29, 2022

Q. In Europe universities and entrepreneurship have a “complicated, love/hate relationship”. What is the way to “make it work”?

A. First of all, Europe does not have a monopoly on this complicated relationship. It exists around the world. Entrepreneurship has not been taken seriously as a field of research and as such the body of knowledge is insufficient for the demand now put on the universities for teaching it. One of the key factors is that research likes clean data sets and it is very hard to get such data sets for new entrepreneurial ventures. Just ask any entrepreneur.

Secondly, the study of business commenced about 150 years ago with the industrial revolution. It focused on how we manage and produce predictable, optimized, and de-risked results. This is the essence of management with things like planning, budgeting, human resource management, financial leverage, supply chain optimization, six sigma quality assurance, and the like. What is common in these things is the assumption of an existing organization. Entrepreneurship is about creation not optimization and derisking. The game is changing.

Academic institutions with tenure, i.e. job for life, or tenure-like arrangements for faculty are, as a result, systems with a lot of inertia. That inertia makes them slow to change and that is what you see right now with the need for the change described above.

Q. A 2015 report about the Entrepreneurial Impact of MIT said that the Alumni-founded companies had created 4.6 million jobs, generating nearly $2 trillion in annual revenues. That would make them the 9th largest economy in the world. What makes MIT-trained entrepreneurs so successful?

A. It is right there in MIT’s motto, “mens et manus,” which translates to “mind and hands.” While others pursue knowledge for knowledge’s sake, a legacy of universities being set up to train clergy and philosophers, MIT’s mission is much different. It is to create a body of knowledge that can be applied to the world’s greatest challenges. As such, this has created a culture of problem-solving. Knowledge by itself is insufficient. It must be applied.

So it starts with the motto and mission and then it builds from there. This has created some initial successes which then creates a virtuous positive reinforcing feedback loop that others see as possible and attempt to do the same. With more success, more people with entrepreneurial tendencies tend to apply and choose to come to MIT which further enhances the entrepreneurial results and so forth. But if you had to point to one thing, it all starts with the DNA from the birth of the institution codified in the motto and mission.

That being said, we have gotten great support to develop a rigorous and relevant innovation-driven entrepreneurship curriculum and associated co-curricular and extra-curricular set of programs to amplify this tendency. MIT has recruited and supports a world-leading set of faculty at the MIT Sloan School of Management who do research on innovation and entrepreneurship. These academic faculty work to make sure we have an evidence-based approach to teaching this important subject. We complement this with highly skilled practicing entrepreneurs to work in tandem with the academic to produce that rigor and relevance we believe is critical to a successful entrepreneurship education program.

Q. Is it that the MIT students and alumni are very entrepreneurial, or do they take cues from their professors?

A. Much less than one would think from the outside. Yes, there are iconic professors like Bob Langer, Dmitri Bertsimas, and Greg Stephanopoulos to name a few who have started multiple companies, but there are also many others who have started none. Professors starting companies is certainly accepted (up to 20% of any professor’s time can be spent on outside activities which may or may not be related to starting a company) but it is not universal. I would argue that MIT has been and will always be a “bottoms up-driven” university rather than a “top-down-driven” organization. That means that the leadership of MIT does not dictate or carefully set directions but rather depends on the drive and creativity coming from the students and faculty. In this case, the students drive entrepreneurship at MIT more than the faculty.

Q. What is needed to help the alumni of Greek universities follow the same steps?

A. I think, first of all, Greek universities need to be supported in increasing their entrepreneurship offerings. The demand for this far exceeds the current capacity. The role of the universities is not to create companies but rather to focus on creating entrepreneurs. There need to be more entrepreneurs and they need to be of a higher quality, what we call innovation-driven entrepreneurs. I would encourage all universities to get, read and take to heart a new book called “From the Basement to the Dome: How MIT’s Unique Culture Created a Thriving Entrepreneurial Community” by Jean-Jacques Degroof. It explains the lessons learned on how to do this but of course, it will need to be adopted to the specific content of each Greek university but it gives a detailed road map as a place to start.

Q. How vital is technology transfer for society?

A. A vibrant technology transfer is a vital part of any university that wants to have an impact. It is the structure and vehicle to move research from the lab to the marketplace. It is important but not the only vehicle. In fact, it is less important than most people imagine. For example, each year at MIT, we have approximately 20-30 companies that are started directly through licenses from the MIT Technology Transfer office. These are very important companies and the office provides a clear path for professors to move their breakthrough ideas to the market for impact. However, each year, MIT and MIT alumni start approximately 1,000 new companies. You can see that the vast majority (97% or more) are not started through the licensing office. This is in no way a bad reflection on the technology transfer but rather indicates if we train students to understand technology, give them a problem-solving mentality and effectively educate them on the entrepreneurial process while instilling them with the proper mindset and way of operating (with a community), the results are less technology-specific than one would imaging.

Q. Is there a formula for a successful entrepreneur? Can you teach someone to be a successful entrepreneur?

A. Interestingly, I would reframe this question. All people are born entrepreneurs and it is then society that slowly dilutes this and even threatens to take it away. From the beginning of time, people survived by making things, trading things, or providing services to people in order to survive.

So an entrepreneurship educator’s job is to bring this back out and then sharpen those skills. There is a lot of empirical evidence that shows entrepreneurship can be learned. The more a person tries entrepreneurship, the more likely they are to be successful. When entrepreneurship is effectively taught, the results are even more compelling. In our full program, ending with the delta v fully immersive educational accelerator, the success rate of our students who start from scratch at the beginning of the process (as measured by whether they are in business five years later) is well over 70%. We also have other data that shows very compellingly that entrepreneurship can be taught.

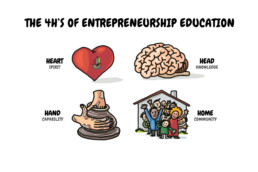

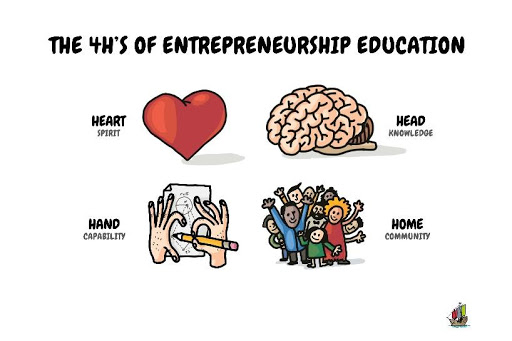

While there is no algorithmic formula to guarantee the creation of a successful entrepreneur and there never will be since success is the achievement of something that is novel and never seen before, there are first principles that dramatically improve the odds of success. Those first principles create the characteristics that we refer to as the 4H’s.

It all starts with the heart and creating the mindset or spirit of being an entrepreneur. This is the joy and drive of being different to make the world a better place. Entrepreneurs not only have the drive to improve over the current status quo, they delight in doing this. Secondly, the successful entrepreneur must understand the first principles of the skills required to achieve their goals. This is the second H, the head. This is the tested body of knowledge that we know improved the odds of success when embarking on an entrepreneurial initiative. This is not from a single source but it is from multiple sources. My just-released book in Greece “Disciplined Entrepreneurship” (check the title here as I believe it has been translated to something more like “Principled Entrepreneurship”) is an excellent example of the first principles. Knowledge alone is not sufficient however to be a successful entrepreneur, it must be conveyed into real-world capabilities. This is the third H, the hand. Since entrepreneurship is a craft, not a science or art, it should be taught in an apprenticeship model. To create entrepreneurs, we must offer co-curricular and extra-curricular programs to supplement the theory we teach in the classroom. Lastly, successful entrepreneurs need to learn how to effectively, efficiently, and quickly access resources beyond their control. This is where the last H comes in, home. For entrepreneurs to increase their odds of success, they need to have a community-based way of operating that is different from the command, control, and conquer approach that is traditionally taught in schools of management.

These are the pillars of our educational program to create high-quality entrepreneurs and it is working as we noted above.

Q. What is the value of organizations like MITEF Greece in cross-pollinating the local communities with the entrepreneurial DNA of the MIT alumni?

A. MIT Enterprise Forum of Greece and similar high-quality organizations play a vital role in creating entrepreneurs and ultimately the companies they create that change the region and world. As noted, entrepreneurship is a craft, and learning it can’t not be done just in a classroom. MIT EF Greece provides the structure and mentors for an apprenticeship model. They also provide invaluable contacts to help the entrepreneurs jump-start their community. In addition, each entrepreneurial journey is unique and the MIT EF Greece can provide the context to apply the first principles. Lastly, the emotional support for something as challenging as entrepreneurship, it is important to have the emotional support of a community like MIT EF Greece to sustain the journey and for the entrepreneur to maintain their mental health. In sum, for these reasons and more, organizations like this are invaluable.

Q. Is innovation-driven entrepreneurship important only for startups? How can large corporations benefit from cultivating the entrepreneurial spirit of their employees?

A. Absolutely not. The Entrepreneurial mindset, skillset, and way of operating should not be confined to startups. Large organizations need entrepreneurs more than ever. Corporations, government, academic institutions, non-profits, and more, need to continue to innovate or they will die out or at a minimum perform suboptimally. As a society, if we are to solve the intractable problems we have in areas like climate change, health care, education, financial inclusion, and much more, we need entrepreneurs everywhere. Startups will only get us the low-hanging fruit. To get the bigger fruit higher up on the trees for areas as I have described above, we will need entrepreneurs in platforms with bigger assets and that means entrepreneurs in large organizations.

Q. What is your advice to Greek universities? Should they be managed by academics or professionals (from the market) in order to succeed in the very competitive global environment?

A. The universities need to be managed by both. As my colleague at MIT, Dean Nelson Repenning, says “My classroom works best when we privilege neither theory nor practice, but instead make sure both are front and center, highlighting where they align and debating the relative merits when they don’t.” It is similar to running a university. We need both academics and practitioners working in harmony to solve the challenge of creating and teaching this new important craft of innovation-driven entrepreneurship.

More specifically, my advice would be to read Dr. Degroof’s book and take it to heart.

Lastly, I would encourage a nationwide effort to make entrepreneurship education something that goes beyond the traditional barriers of a universities’ walls. They should partner with the government and organizations like MIT EF Greece to create an annual Grand Entrepreneurship Prize with extensive programming to support it. The programming that is now possible through online classes presents exciting opportunities to make their content, which has been historically only available to a select few, more broadly available to everyone in Greece. MIT EF Greece could help with the outside the university programming, in collaboration. The government could play a powerful role in marketing, financial support, and brokering across different stakeholder groups. I encourage the universities, and others, to think more ambitiously. If we are to survive and thrive, and I would argue if democracy is to survive and thrive, we need to create not thousands more entrepreneurs but millions. Then we will give all Greeks the opportunity for hope and pride in their lives and true incentives for rigor. It is not only possible but Greece would be the ideal place to implement such a plan.

Q. How much did the pandemic affect universities? Do you see in your students a difference in their behavior or their performance?

A. The pandemic just accelerated the need for entrepreneurship education and reinforced the notion that is relevant beyond just startups. The disruption to our lives and the creative thinking required to survive, solve and come out stronger on the other side, clearly illustrated the value of having people with an entrepreneurial mindset, skill-set, and way of operation. We will never go back to our old ways. Looking at the long arc of history, we know that the rate of change will continue to accelerate. In such a world, entrepreneurs are needed more than ever – throughout all of society. That became crystal clear more than it ever had before. We cannot go back to the old ways. Students feel this and want entrepreneurship more than ever. Faculty and administrators know it. We welcome the challenge but it will not be easy. We need to work more collaboratively than we ever have before and embrace the uncertainty. In other words, act like entrepreneurs ourselves.

The author

Bill Aulet

A longtime successful entrepreneur, Bill is the Managing Director of the Martin Trust Center for MIT Entrepreneurship and Professor of the Practice at the MIT Sloan School of Management. He is changing the way entrepreneurship is understood, taught, and practiced around the world.

The books

This methodology with 24 steps and 15 tactics was created at MIT to help you translate your technology or idea into innovative new products. The books were designed for first-time and repeat entrepreneurs so that they can build great ventures.